News

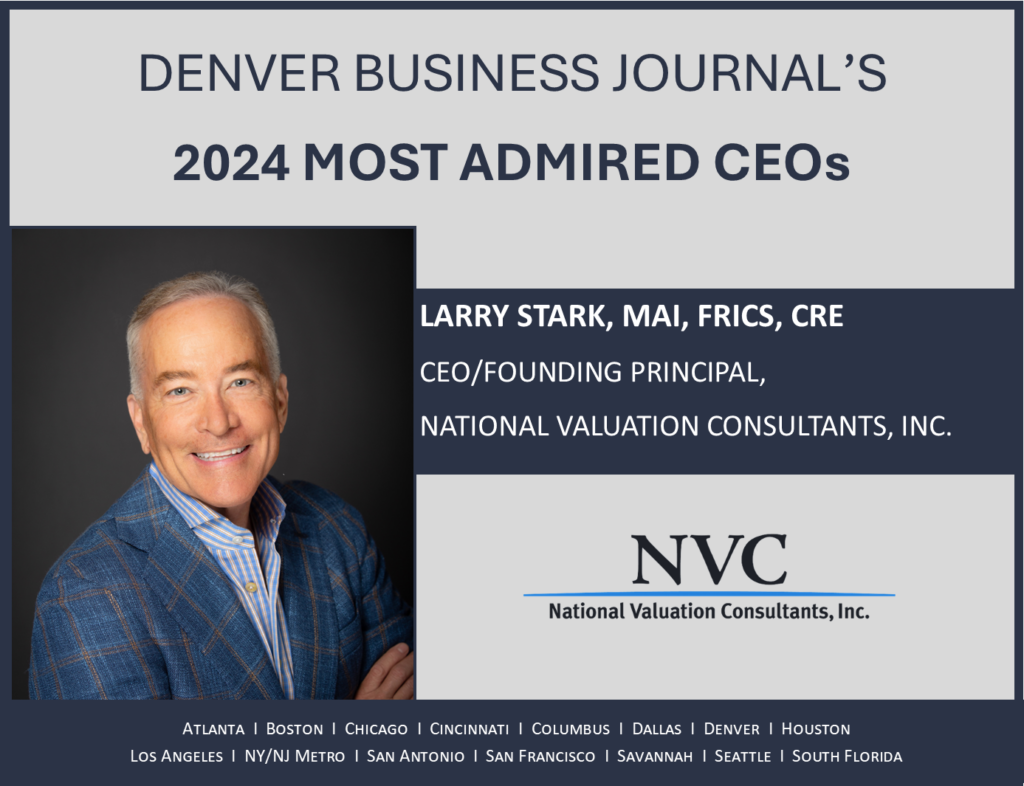

Congratulations to CEO and Founding Principal, Larry Stark, on being named one of the Denver Business Journal’s 2024 Most Admired CEOs. Your vision, leadership and commitment to your employees, clients and the community have guided NVC to its success as a highly respected commercial real estate and consulting firm.

We are thrilled to announce that NVC has been named a Top Workplace for a third year! Thank you to our entire staff – nationwide – for continuing to make NVC such a great place to work.

We are excited to announce that NVC has been named a “Best Place to Work” finalist by the Denver Business Journal. We share this honor with all of our employees whose dedication to providing expertise and best-in-class service to our clients has helped us grow to be the largest privately held commercial real estate appraisal firm in the country.

NVC’s Chuck Dannis Named to the 2023 Dallas 500

We are proud to announce that Chuck Dannis, Senior Managing Director of NVC’s Dallas office, has been named to the 2023 Dallas 500 – celebrating the most influential leaders in North Texas. We are thrilled that Chuck has been awarded this well-deserved honor, and are grateful for his many contributions to our firm, the commercial real estate industry and the community.

NVC’s Chuck Dannis Discusses Texas Commercial Real Estate and the Changing Capital Markets Environment

Chuck Dannis, Senior Managing Director of NVC’s Dallas office, sits down with prominent tax consultant Paul Pennington of P.E. Pennington & Company in a “PEP Talk” podcast (already seen by over 30,000 viewers), where they have a head to head, deep dive discussion into Texas commercial real estate and the rapidly changing capital market.

National Valuation Consultants wins “Top Company” Honor

NVC is thrilled to be recognized by ColoradoBiz magazine as the “Top Company” in the professional services category. The annual awards program recognizes Colorado’s outstanding businesses through a challenging and rigorously judged competition based on outstanding achievement, financial performance and community involvement.

We share this honor with each of our 120 talented employees nationwide who provide best-in-class service and commercial real estate expertise to our clients.

Examining the Texas Triangle through the commercial real estate lens

By Anna Butler – Real Estate Editor

Dallas Business Journal – September 7, 2022

Inspired by “The Texas Triangle: An Emerging Power in the Global Economy,” National Valuation Consultants Inc. set out to apply the key principles of the 2021 book to the commercial real estate sector, focusing on data and trends tied to rent, vacancy and inventory levels for multifamily, industrial, retail and office.

The key takeaways of NVC’s research? Both the projected influx of new residents and an economy that is better-insulated from market forces are expected to continue to catapult the region forward. For a link to the Dallas Business Journal article, click here.

For a link to NVC’s in-depth research article “Commercial Real Estate in The Texas Triangle”, click here.

National Valuation Consultants wins Best Places to Work honor

By Allison Shirreffs – Contributing Writer

Atlanta Business Chronicle – September 2, 2022

National Valuation Consultants Inc. is ranked No. 2 on Atlanta Business Chronicle’s 2022 Best Places to Work list in the Small Company (10-49 employees) category.

When the pandemic first started, Peter Lamas, senior managing director, National Valuation Consultants Inc. (NVC) watched as his contacts in commercial real estate tried to figure out the long-term effects on the industry. Given that NVC is the largest privately held commercial real estate appraisal firm in the U.S., providing a wide range of appraisal, valuation management, consultation and real estate advisory services, the implications were huge.

Though the commercial office sector remains sluggish, industrial and multifamily real estate took off in the second quarter of 2021. According to Colliers, the Q2 2022 vacancy rate was 3.4% for industrial real estate in metro Atlanta. Nationwide, J.P. Morgan’s 2022 midyear commercial real estate outlook pegged multifamily vacancies at 4.7% as of Q1 2022. Strong markets mean more work for NVC, and the company is currently operating at 125% capacity. Recent increases in the Federal Reserve interest rate cooled things a bit, but Lamas, who’s been in the industry for 30 years (10 of those in Atlanta with NVC), said he’s never seen the market this hot. <Read Full Article>

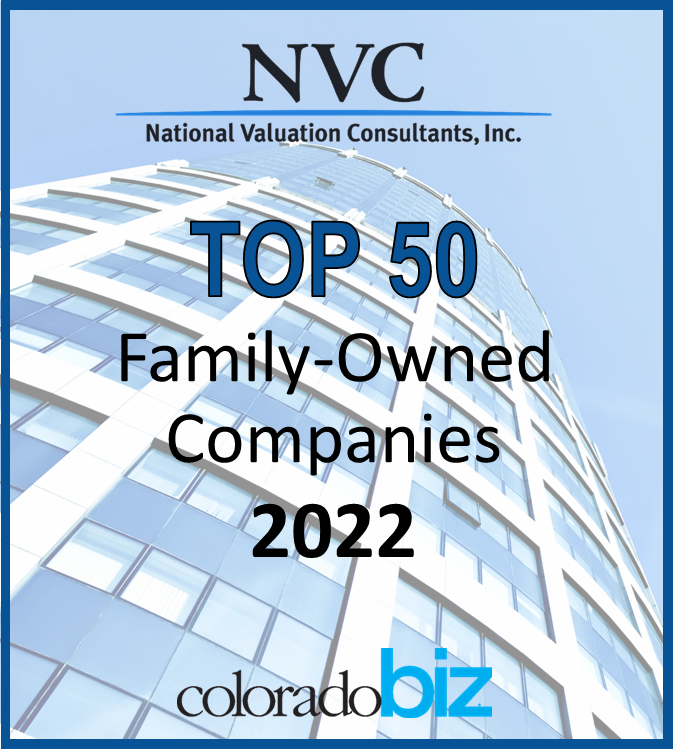

NVC is proud to be recognized as one of the Top 50 Family-Owned Companies in the latest issue of ColoradoBiz Magazine. Celebrating 30 years of Excellence as a national provider of commercial real estate valuation and advisory services.

Congratulations to two members of NVC’s Dallas valuation team, John Scarborough, SRA and Alex Yakulis, MAI who were recognized last week for their many contributions to the North Texas Chapter of the Appraisal Institute. Alex, who currently sits on the AI Board, was recognized as the 2021 Volunteer of the Year and John was honored with the prestigious Lifetime Service Award for his more than 15 years of contributions and service.

Congratulations, and thank you for your service and contributions to the appraisal industry.

NVC Celebrates a Milestone!

We are thankful for our clients who have supported us over the last 30 years, helping us to grow into the largest privately held commercial real estate appraisal and consulting firm in the U.S.

We are also grateful to our amazing staff who have helped us achieve our success by carrying on our firm’s commitment to excellence.

Atlanta Business Chronicle – July 21, 2021

NVC is thrilled to share the news that our firm has been recognized as a 2021 “Best Place to Work” by the Atlanta Business Chronicle. This honor carries special significance, as it is based upon employee feedback gathered through an anonymous third-party survey that measures several aspects of workplace culture including employee engagement, effectiveness of leadership, and job satisfaction. Earning this accolade is the result of adhering to our company values which revolve around putting people first, pursing excellence, acting with integrity, and serving our community.

Established in 2003, NVC’s Atlanta office is led by Peter Lamas, MAI, who has been instrumental in the growth of the office’s staff and clientele, leading it to be ranked as Metro Atlanta’s second largest Commercial Real Estate Appraisal Firm by the Atlanta Business Chronicle in 2020.

For more information about Career Opportunities with our firm, click here.

NVC’s Alex Yakulis Awarded MAI Designation

NVC is pleased to announce that Alexander G. Yakulis IV was recently awarded the MAI designation by the Appraisal Institute, representing advanced knowledge, proven valuation experience and a commitment to strict professional standards and ethics. Alex, who has more than 10 years of commercial appraisal experience serves as a Senior Vice President in NVC’s Dallas office, where he is involved in the valuation of all types of commercial properties, with a focus on property tax appeal and litigation support. He is also actively involved in the North Texas Chapter of the Appraisal Institute, where he serves on the Board of Directors and participates on various committees.

NVC is pleased to announce that Alexander G. Yakulis IV was recently awarded the MAI designation by the Appraisal Institute, representing advanced knowledge, proven valuation experience and a commitment to strict professional standards and ethics. Alex, who has more than 10 years of commercial appraisal experience serves as a Senior Vice President in NVC’s Dallas office, where he is involved in the valuation of all types of commercial properties, with a focus on property tax appeal and litigation support. He is also actively involved in the North Texas Chapter of the Appraisal Institute, where he serves on the Board of Directors and participates on various committees.

NVC Honored as a 2021 Top Workplace

NVC Honored as a 2021 Top Workplace

The Denver Post – May 5, 2021

NVC is excited to announce that we have been awarded a Top Workplaces 2021 honor by the Denver Post. The award is based solely on employee feedback gathered through an anonymous third-party survey that measures several aspects of workplace culture. As stated by CEO and Founding Principal, Larry Stark, “We share this honor with all of our employees who give us our competitive advantage, create our culture and provide the foundation of our continued success.“

Click here to view our online profile.

NVC’s Robin Schween Honored as one of 2021’s Most Influential Young Professionals

ColoradoBiz Magazine – March 5, 2021

NVC is proud to announce that Managing Director, Robin Schween, was among the GenXYZ finalists selected by ColoradoBiz magazine, honoring 2021’s Most Influential Young Professionals. The award recognizes young professionals aged 21-39 who are using their youthful energy to take care of business and are helping to shape the next generation of Colorado’s economy. We are grateful to Robin for his leadership, passion for serving our clients and for the many contributions he has made to our firm, the industry and our community.

Congratulations Robin – Well Deserved!

Retail Investment’s Lonely Bright Spot: Triple-Net Assets

Retail Investment’s Lonely Bright Spot: Triple-Net Assets

By Connor Hoagland, Associate – National Valuation Consultants, Inc.

Colorado Real Estate Journal – October 7, 2020

Retail has it tough. In the commercial real estate investment world, retail has been the industry pariah ever since the big, bad online retail phenomenon moved to the block. And then, as if retail investment could get much worse, COVID-19 happened. Mandated stay-at-home orders, business closures, and a general hysteria of close personal contact has affected the retail sector for the foreseeable future. With high volatility in the marketplace, investors are looking for safe, durable investments. Don’t look now, but could the safe haven for investors actually be hiding out within the withering retail segment? Single-tenant triple-net assets historically have been a mainstay for investors looking for steady income and mitigated risk. Now might be the perfect time for triple-net retail to shine. <Read Full Article>

Retail has it tough. In the commercial real estate investment world, retail has been the industry pariah ever since the big, bad online retail phenomenon moved to the block. And then, as if retail investment could get much worse, COVID-19 happened. Mandated stay-at-home orders, business closures, and a general hysteria of close personal contact has affected the retail sector for the foreseeable future. With high volatility in the marketplace, investors are looking for safe, durable investments. Don’t look now, but could the safe haven for investors actually be hiding out within the withering retail segment? Single-tenant triple-net assets historically have been a mainstay for investors looking for steady income and mitigated risk. Now might be the perfect time for triple-net retail to shine. <Read Full Article>

Most Admired CEO Matt Ansay Builds Consensus at Workplace and Within Industry

Most Admired CEO Matt Ansay Builds Consensus at Workplace and Within Industry

By Jonathan Rose – Associate Editor

Denver Business Journal – November 16, 2020

2020 marks Denver Business Journal’s third consecutive year of recognizing outstanding top executives at businesses within the region – and it’s happening at a time when strong, visionary leadership is more important than ever before.

The 2020 Most Admired CEO program honors top-ranking execs who are guiding their companies through the unprecedented challenges posed by the Covid-19 pandemic, and whose past success is evident in the enduring strength of the companies they lead.

Click here to read the full profile on Matt which includes a short video discussing his favorite fictional superhero.

NVC Ranked Second Largest CRE Appraisal Firm in Atlanta

NVC is proud to announce that our Atlanta office, managed by Peter Lamas, MAI has been recognized as Metro Atlanta’s second largest Commercial Real Estate Appraisal Firm by the Atlanta Business Chronicle. Firms were ranked based on total dollar volume appraised by each firm’s local Atlanta-based office.

NVC is proud to announce that our Atlanta office, managed by Peter Lamas, MAI has been recognized as Metro Atlanta’s second largest Commercial Real Estate Appraisal Firm by the Atlanta Business Chronicle. Firms were ranked based on total dollar volume appraised by each firm’s local Atlanta-based office.

“This accomplishment is a testament to the outstanding leadership and work ethic of our Atlanta office, and the ongoing commitment by our entire valuation team to delivering expertise, integrity and transparency along with top-notch client service on every assignment. Congratulations to our Atlanta team!”

– Larry Stark, MAI, CRE – Founder/CEO

NVC Recognized as a “Top Company” Finalist by ColoradoBiz Magazine

NVC is proud to have been recognized as a finalist in ColoradoBiz Magazine’s “Top Company” awards within the Professional Services category, which we share with and attribute to the wonderful team of dedicated professionals that make up our firm.

Contenders were judged in a number of categories including each company’s outstanding achievement, community involvement, challenges faced and overcome, company culture, competitive advantage, future goals and financial strength. Following is an excerpt from the September 6, 2020 article by ColoradoBiz’s Lisa Ryckman highlighting NVC. Click here for a link to the full article.

National Valuation Consultants

Denver

Founded in 1991, National Valuation Consultants, the nation’s largest privately held commercial real estate valuation and advisory firm, has grown from a single office of five in Denver to eight offices across the country.

NVC provides a broad range of appraisal, consultation and real estate advisory services, including commercial real estate appraisal and appraisal review, valuation management services and debt valuation, among others. In 2019, NVC served 526 clients, completing more than 8,400 valuation and advisory assignments on a wide array of property types valued at more than $500 billion.

NVC’s 100 employees benefit from a wellness committee that promotes company-wide programs and initiatives for a healthy work-life balance and community partnerships. Team members and their partners from all NVC offices gather annually in January to reflect on the year and celebrate individual and company-wide events, milestones and achievements.

Matthew D. Anderson, MAI, AI-GRS

Garrett Gerstung, MAI, AI-GRS

NVC is proud to announce that two senior members of our Atlanta office, Matt Anderson and Garrett Gerstung, recently earned the AI-GRS designation from the Appraisal Institute.

Award of this additional credential, pursued by professionals who provide reviews of appraisals on a wide range of property types, requires meeting rigorous education requirements and passing a comprehensive exam. Both valuation team members have been with NVC for more than 10 years, and have extensive experience with all types of income producing properties and vacant land throughout the United States as well as more specialized assets including cold storage.

Coworking: Is it here to stay or time to vacate?

Coworking: Is it here to stay or time to vacate?

By Will Fehr, Associate – National Valuation Consultants, Inc.

Colorado Real Estate Journal – Office Properties Quarterly – September, 2020

If you asked people involved in the coworking space during the first half of 2019 what their long-term outlook was for the industry, it would have been overwhelmingly positive. WeWork, the nation’s largest coworking operator, was on a tear leasing up several spaces in the greater Denver area. In fact, even still it is Denver’s largest landlord with nine Denver locations totaling approximately 570,000 square feet, plus an additional 30,000 sf office space in Boulder. Other coworking companies, such as Regus and Novel Coworking, also have been expanding their footprints. Between the three biggest coworking companies alone, they occupy more than 1.3 million sf of office space in Denver.

If you asked people involved in the coworking space during the first half of 2019 what their long-term outlook was for the industry, it would have been overwhelmingly positive. WeWork, the nation’s largest coworking operator, was on a tear leasing up several spaces in the greater Denver area. In fact, even still it is Denver’s largest landlord with nine Denver locations totaling approximately 570,000 square feet, plus an additional 30,000 sf office space in Boulder. Other coworking companies, such as Regus and Novel Coworking, also have been expanding their footprints. Between the three biggest coworking companies alone, they occupy more than 1.3 million sf of office space in Denver.

Fast forward to today, and the office climate is dramatically different. Clearly the onset of the pandemic has altered demand for office space, but even prior to the disruption caused by the novel virus, WeWork was already in trouble. 2019 was a bad year for the co-working giant as it featured a failed initial public offering bid in mid-September, a multibillion-dollar bailout from SoftBank in October, negative press surrounding leadership failures and significant layoffs. The public health crisis of 2020 could not have come at a worse time for the once-promising unicorn. As of this writing, it has backed out of a deal to occupy four floors in an office in Uptown, it is no longer pursuing space at McGregor Square, and it has removed its consideration for leasing space at Junction23. And it’s not just WeWork that is struggling; The Riveter and Charley Co., two women-oriented coworking spaces in River North that opened in July 2019, announced they will permanently shut down due to the pandemic.

Government-mandated shutdowns for the State of Colorado were implemented in March and lasted for two months. It was not until early May that Gov. Jared Polis stated that offices could gradually reopen at 50% capacity. Although restrictions have eased, countless companies have chosen to drastically delay going back to work. As employees have proven that their overall efficiency and work capabilities are not negatively impacted by working from home, some office users have even announced permanent work-from-home strategies. For coworking specifically, the challenges are intensified since open floor plans and coworking office spaces are, by definition, not conducive to social distancing. And while all operators are employing increased cleaning schedules and have de-densified spaces, the concern of working in proximity to others wins the day.

So, is co-working dead? While the road to recovery is steep, there are a few reasons why co-working could survive, or even thrive, in the years to come under our “new normal.” First, the decline in office demand with more workers staying home could trigger downsizing of office space for some Denver-based companies. As more businesses continue to work from home effectively, their need for large amounts of office space decreases. Will coworking capitalize on this opportunity with the ability to lease smaller amounts of space to downsizing users? Second, coworking space can offer flexible lease terms that may appeal to tenants with upcoming expirations who may choose to seek a shorter term rather than being locked in for a long period of time given the uncertainty caused by the pandemic. In this time of uncertainty, flexible lease terms are a benefit many companies are seeking. Rather than signing a five- to 10-year lease, businesses can lease space at a coworking facility on a monthly basis. The coworking model allows enterprises to add or subtract from the number of desks they occupy, which simplifies hiring and scaling.

As employees demand a more flexible work schedule and environment, coworking continues to offer an adequate solution. As employers realize that large amounts of office space are no longer needed to support business operations, coworking could fill that need. However, for coworking to survive, the business model may need to adjust to attract the more established businesses that rely on the flexibility that is vital when economic uncertainty affects hiring and growth plans. For example, imagine the established firm that needs to expand its total office footprint to allow for more spacing within its office by supplementing with multiple coworking spaces in strategic locations near employees’ homes. A hybrid approach of traditional office space, coworking and home may fit well into the future of office demand. So while the last several months may suggest that coworking is a dying industry, don’t count it out just yet. There could be a lot more fight in it.

Residential resilience in Denver: Prices continue to surge

By Julian Factor, Senior Associate – National Valuation Consultants, Inc.

Colorado Real Estate Journal – September 2, 2020

Over the last decade, Denver has been regarded as one of America’s best residential real estate development markets. The seven-county metropolitan area (Adams, Arapahoe, Boulder, Broomfield, Denver, Douglas and Jefferson counties) has experienced a migration boom from other regions of the United States with the total population reaching nearly 3.3 million residents, an annual increase of 1.7% since 2010. Residents would agree that there always seems to be a new apartment building, condominium, or custom home being built just down the street. Indeed, for years the housing inventory in metro Denver has struggled to keep pace with demand. Land developers have been buying developable land at a rapid pace, pumping out finished lots and vertical improvements with the market’s rapid absorption easily covering any potential overbuilding. For example, as recently as the first quarter, there were more than 200,000 planned residential lots in the Denver metropolitan market. In terms of economic equilibrium, demand has not been the issue in these recent years of expansion; supply has long been the limiting factor.

Over the last decade, Denver has been regarded as one of America’s best residential real estate development markets. The seven-county metropolitan area (Adams, Arapahoe, Boulder, Broomfield, Denver, Douglas and Jefferson counties) has experienced a migration boom from other regions of the United States with the total population reaching nearly 3.3 million residents, an annual increase of 1.7% since 2010. Residents would agree that there always seems to be a new apartment building, condominium, or custom home being built just down the street. Indeed, for years the housing inventory in metro Denver has struggled to keep pace with demand. Land developers have been buying developable land at a rapid pace, pumping out finished lots and vertical improvements with the market’s rapid absorption easily covering any potential overbuilding. For example, as recently as the first quarter, there were more than 200,000 planned residential lots in the Denver metropolitan market. In terms of economic equilibrium, demand has not been the issue in these recent years of expansion; supply has long been the limiting factor.

Data gathered by Metrostudy shows that Denver has seen more than 12,075 new annual home starts since this time last year. Even so, the months of inventory for new finished vacant product is only 1.4 months compared with a healthy market of 3.2 months as defined by Metrostudy. With all this pent-up demand, Colorado has attracted developers to purchase enormous portions of residential land. Then the COVID-19 pandemic hit, sending markets into a tailspin and causing uncertainty in the residential markets throughout the country. There was so much uncertainty at the time that the Federal Reserve lowered its benchmark interest rate in March so potential home buyers would be incentivized to purchase. While unemployment, empty office buildings and shuttered retail stores have precipitated a halt in the residential market in many U.S. municipalities, Denver’s seven-county metro residential market mostly has maintained its pre-COVID-19 momentum.

It is hard to imagine that Denver’s residential market maintains this level of success even as other sectors of commercial real estate industry languish in the COVID-19-impacted market. Take Denver’s office market, for example, where occupancy is declining and where total transaction activity decreased by 6% since 2019. Further, office subleases are on the rise and currently account for 1.5 million square feet of leasable area, up 15% from April and nearly 70% higher than the same time one year prior. As a leading indicator, this may indicate that the office market has peaked, and rental rates may begin declining. However, for residential developers, there is a silver lining to the pain in the current commercial market. As more companies adopt the work-from-home structure, thereby giving their employees more flexibility with regard to housing, and as traditional central business district office tenants signal their intent to abandon the high-density downtown locations in favor of low-density suburban options, homebuyers’ preferences are evolving to favor the outlying suburban communities.

We spoke with residential land developers prominent in metro Denver who indicated that though the industry experienced some disruption, they do not intend to change their prepandemic business plans. While their offices experience the typical slowness, construction is considered an essential business and it continued to operate through most of Colorado’s stay-at-home orders. And while transaction volume slowed in the months of February and March, most developers still were keen on purchasing available raw land and finished lots. One interviewed homebuilder quipped that general issues with regards to construction, design and development were slowing production more so than the pandemic.

Available home inventory still is near historic lows in the urban areas, driving extremely strong price gains, according to reColorado. As prices continue to reach all-time highs, many first-time buyers find themselves priced out of the market as new development in the urban infill areas has concentrated at the higher end of the price range. Since the average price of a home across the seven-county metro is $457,000, a 20% down payment on a home means a buyer should be looking to spend more than $91,000. While developers do contribute portions of their land for the benefit of the community, such as constructing dedicated school sites or affordable housing, demand is too strong to keep prices down. Unfortunately for low-income earners, the price trajectory is still sharply upward.

This positive trend of sales activity in Denver is also true for urban-infill attached product such as condominiums and townhomes. In some cases, this type of product is experiencing greater price surges when compared to single-family development. In fact, attached-product developers are reporting strong presales activity, and some are having to limit the number of presales over the construction period. Though sales activity for condominiums and townhomes have decreased in 2018 and 2019, this decline was largely attributed to the lack of overall availability and, despite these fluctuations, average sales price for condominiums rise at an average of 8% a year. In 2019, the average sales price for condominium was listed at $346,494 – a 7.4% increase over 2018. Due to limited availability, sales trends for attached-product in Denver is operating similar to the single-family market.

A lender with one of Colorado’s banks indicated that their current perception of risk on new transactions is relatively low. Though financing briefly halted between February and April, there is still an appetite for financing according to the lenders who participated in our survey. In fact, many lenders pointed to the developer concern about Colorado’s construction defects law as a more pressing issue than the pandemic. As though hedging his bet, one lender did note that the currently strong housing prices may weaken if the virus lasts longer than expected, and unemployment levels remain elevated through the year. Nonetheless, the ubiquitous perception among residential lenders is that financing of development projects will continue.

Despite national concerns regarding the ongoing pandemic, the overall outlook of the residential market in metro Denver is favorable. The insufficient supply of housing will remain a core issue with regards to affordability, and it appears that it will take a bigger disruption than COVID-19 to interrupt this healthy market. Additionally, with the recent disruption of the office market, homebuyers are now more likely to purchase outside the core Denver area. Residents should expect to see a continued expansion new urban and suburban neighborhood throughout metro Denver for years to come.

The Gallagher Amendment and Colorado’s tax landscape

By James Simpson, Associate – National Valuation Consultants, Inc.

Colorado Real Estate Journal – August 4, 2020

Since its 1982 enactment into the Colorado State Constitution, the Gallagher Amendment has served as the balance for which residential and non-residential property taxes are distributed. At its core, the amendment stipulates that residential assessments can comprise no more than 45% of the state property tax base, while non-residential (commercial, industrial, vacant & agricultural land, natural resources, and state assessed property) make up the remaining 55%. Further, under the amendment, non-residential assessments remain fixed at 29% of market value, while the residential rate “floats” so that the 45% and 55% split is upheld. In other words, the residential assessment rate is the lever by which the Gallagher equation is held in balance. However, Colorado lawmakers are increasingly crying “foul” as the intended balance is placing a disproportionate burden on businesses, overly stressing municipal budgets and forcing officials to make deep cuts to already challenged local community resources. How did we get there? Let’s take a moment to explain.

Since its 1982 enactment into the Colorado State Constitution, the Gallagher Amendment has served as the balance for which residential and non-residential property taxes are distributed. At its core, the amendment stipulates that residential assessments can comprise no more than 45% of the state property tax base, while non-residential (commercial, industrial, vacant & agricultural land, natural resources, and state assessed property) make up the remaining 55%. Further, under the amendment, non-residential assessments remain fixed at 29% of market value, while the residential rate “floats” so that the 45% and 55% split is upheld. In other words, the residential assessment rate is the lever by which the Gallagher equation is held in balance. However, Colorado lawmakers are increasingly crying “foul” as the intended balance is placing a disproportionate burden on businesses, overly stressing municipal budgets and forcing officials to make deep cuts to already challenged local community resources. How did we get there? Let’s take a moment to explain.

When initially implemented, the residential assessment rate began at 21%. This has since plummeted to the current 7.15% rate, due primarily to the significant growth and subsequent residential value boom across metropolitan Denver. As a result, the marked decline in the residential assessment rate has resulted in roughly $35 billion in tax relief to Colorado homeowners since 1983. While the average front range homeowner may be unaware of these tax benefits due to the recent meteoritic rise of front range home values, it is the rural areas of Colorado where, much to the homeowner’s delight, the effects of the Gallagher Amendment have been most pronounced. According to Michael Van Donselaar, Director of Property Tax at Duff and Phelps, rural areas of Colorado depend heavily on activities such as natural resource extraction, and unlike the Front Range where values have spiked since the recession, the same has not held true in such rural parts of the state. Furthermore, sustained business activity across the Front Range has hedged against residential property tax cuts; however, for more rural areas that have experienced far less growth, the combination of stagnant residential values and declining residential assessment rates (which are uniform statewide regardless of one’s location) has resulted in a significant reduction to tax revenue at the local level.

Now 38 years after becoming law, the Colorado legislature is once again attempting to repeal Gallagher (a repeal effort in 2003 failed by a large margin). However, following the recent approval from both the House and the Senate, the November 2020 ballot will be the first opportunity for Colorado residents to have their final say on the issue.

If a repeal were successful, Mr. Keith Erffmeyer, the Denver County Assessor, said that the specific tax landscape post-repeal remains speculative. According to Erffmeyer, what is known is that a repeal of the Gallagher Amendment would effectively freeze assessment rates at 7.15% (residential) and 29% (commercial) due to a companion bill, Senate Bill 223, that accompanied the recent approval. Future legislation could alter these rates; however, the Tax Payer Bill of Rights would prevent any increases in the assessment rates without a subsequent vote from Colorado residents.

Conversely, should Colorado residents vote down the repeal, Erffmeyer echoed the fear espoused by the bipartisan legislature currently promoting the repeal efforts; namely, the residential rate could continue to decline as a result of sustained home value increases, while the COVID-19 pandemic places historic downward pressure on non-residential (commercial) values. The result? The state’s property tax administrator estimates a residential rate decline from 7.15% to 5.88%, which would render a $491 million cut for school districts statewide and a $204 million cut for county governments. All this in a time where businesses are failing, and government coffers are reeling.

To date, the 5.88% estimate for the residential rate is just that, an estimate. However, since residential and non-residential property types are reassessed in odd-numbered years, the waning effects of COVID-19 on the real estate assessment landscape could make the 2021 reassessment that much more challenging, whether or not the Gallagher Amendment repeal survives. It is important to note that 2021 assessed values will be based on an effective date of June 30, smack at the tail-end of the COVID-19 pandemic. Those familiar with the current commercial real estate market are aware that COVID-19 has stalled many commercial real estate transactions, as the gap between buyer and seller expectations of value widens. The result has been a dearth of sales data leading up to the June 30 date of value. While many professionals within commercial real estate valuation acknowledge a decline across commercial values during the pandemic, obtaining substantive sales data to prove this assertion creates quite a conundrum for assessors in the upcoming reassessment cycle.

Unfortunately, once the COVID-19 pandemic subsides and normal market activity resumes, sales that occur beyond the effective date of value and assumedly point towards a general decline across commercial values (some property types presumably faring better than others), could trigger a record number of appeals from building owners come spring of 2021 when the assessed values are released, notes Erffmeyer. He revealed that several plans are being considered to combat the potential issue, though none are concrete enough to report at this time.

While there are many arguments for and against the prior effectiveness and future appropriateness of the Gallagher Amendment, there’s little debate that the current pandemic is putting local municipalities in a tough spot. Without question, the efficacy of the Colorado legislator’s repeal efforts will impact Colorado’s commercial real estate landscape for years to come and, while several different outcomes are possible, the sustained burden that Gallagher continues to place on local government and community resources should make a caution case for the voting public to at least consider the repeal.

How COVID-19 has Changed this Year’s Summer Travel Plans

By Will Fehr, Associate – National Valuation Consultants, Inc.

Colorado Real Estate Journal – July 15, 2020

It comes as no surprise that in the midst of the ongoing COVID-19 pandemic the hospitality industry has struggled mightily with the sharp reduction in nonessential travel. From vacant hotel parking lots to frequent notices of cancelled conventions, the anecdotal evidence is clear. Even more clear is the actual evidence of an ailing industry: According to the June 13 weekly report published by Smith Travel Research, hotel occupancy in the U.S. was 41.7%, as compared to 73.7% in the same week in 2019, a 43.4% drop. Further, the average daily rate of $89.09 is 33.9% lower and revenue per available room is $37.15, a 62.6% decline from the same period in 2019.

Based on statistics compiled by the Metro Denver Economic Development Corp., local figures specific to the metro Denver region paint an even more dire picture as the local average hotel occupancy rate fell 59.3% year over year to 15.7% in the month of April (most recent data available). For the same period, the average daily hotel room rate fell to $84.38, a decrease of $57.24 per night.

And it’s not just hotels. Convention centers remain vacant. Some casinos have gone dark. Local excursions are cancelled, and airlines have cut multiple routes. Denver International Airport reported only 299,000 total passengers in April and 13.33 million total passengers year-todate 2020, a staggering decrease of 94.4% and 34.3%, respectively, from the same periods the prior year.

So, cancel the summer vacation. Call off the reunions. Might as well home school through the summer. Right? Not so fast, says one enclave of the travel industry. Let’s go RVing!

In the face of the overwhelming negative data facing hospitality, travel and recreation, the recreational vehicle industry has seen an uptick in demand and a newfound opportunity to gain market share. With safety being top of mind during this time, most vacationers are choosing to hit the road rather than the skies.

“Due to fears associated with high-density travel via airplanes and cruise ships, it is expected that COVID-19 will lead to an increased interest in RVing due to its inherent ability to promote social distancing. This conclusion is also further supported by the recent surge in RV rental and sale demand,” stated an asset manager with a national portfolio of RV camping sites and manufactured housing communities with transient sites available to RV owners.

According to a study conducted by Kampgrounds of America, 34% of prospective U.S.- and Canada-based campers say that road trips will be the safest form of travel as stay-at-home orders have been lifted. Amid coronavirus concerns, the RV Industry Association also found that 20% of U.S. residents surveyed have become more interested in RV travel versus flying, tent camping, cruises or rental stays.

As many states throughout the union gradually have lifted stay-at-home orders, RV dealers have seen a sharp increase in purchases. Thor Industries, one of the largest manufacturers of recreational vehicles in the U.S., has seen increases in RV sales over the past couple of months as evident by its Airstream line, which reported an 11% increase in sales between May 1 and May 21 as compared to the same period last year. Moreover, a recent study by Thor indicates that 39% of people surveyed said they would be using their RVs more often this year. The study also found that 78% of potential RV-ers will purchase a RV this year, while 18% of current RV owners also will be purchasing another RV.

Importantly, the state of Colorado could be set to benefit from this new shift in vacationing preferences as it contains several National Parks, campgrounds and RV sites, and is widely known for its outdoor activities. On May 11, Colorado Parks and Wildlife announced plans to start opening the state’s parks and campgrounds. In addition, Rocky Mountain National Park began welcoming visitors on May 27. The park has opened approximately 60% of the park’s maximum parking capacity or 4,800 vehicles (13,500 visitors) per day.

But it isn’t only the state and national parks taking advantage as the private sector also is benefiting. In speaking with representatives at Winding River Resort RV Park in Grand Lake, management stated that overall reservation activity has been “through the roof.” Since reopening in mid-May, it has been operating at or near full capacity despite being unable to conduct its normal food services. Most summer weekends are fully booked, and the resort is even getting reservations for next year. Similarly, Management at the Cripple Creek KOA in Cripple Creek indicated that total RV reservations for June are up a total of 11% compared to the same time last year. While July reservations are only up 4% year over year, August reservations have increased by a massive 43%.

Although the COVID-19 pandemic has resulted in considerably less air travel and fewer hotel stays, the underlying desire for travel has not gone away. Rather, it has caused travel demand to shift from airlines and hotels to RVs and campgrounds. So, while owners and shareholders within the hospitality and travel industry stand on the sidelines with legitimate concerns about the future of travel, growth in RV usage has created a boon for recreation vehicle manufactures, owners of RV resorts and manufactured housing communities with transient sites and amenities. Resort property owners are poised to reap the benefits as demand drives increases to reservation fees and monthly lease rates. So don’t call off the summer vacation quite yet. Fire up the old RV, pull the wheel chocks and let’s roll!